For some strange reason, I have a lot of fun in tracking and managing finances. I was taught young to save and invest, and the flexibility that being consistent there will enable. While I’ve got some opportunities to do the investing piece better, I think I’ve got the savings part down pretty good. The biggest (but not only) independent savings contributions I make are through my employer 401k. There’s lots of great things here, but the best single part is the substantial employer matching.

In 2025, I contributed a total of $41,636.16 (!!!) and the best part is I didn’t have to do it alone (thanks company match!)

What makes up these savings contributions?

There is a maximum individual contribution allowable. In 2025 that was $23,500, or almost $2,000 a month. In 2026 this increases to $24,500.

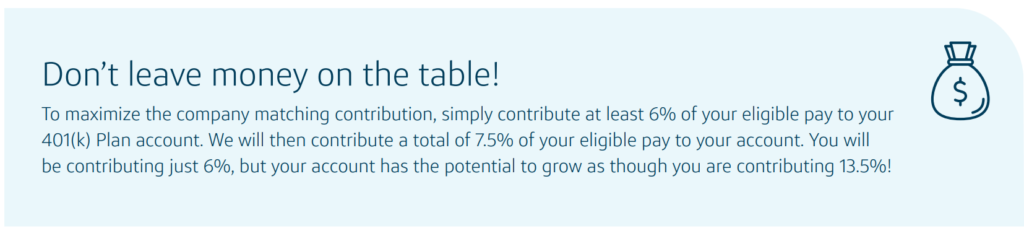

My own (and many other) employers offer substantial matching of funds, as an incentive for individuals to contribute. In 2025, for me this was $18,136.16. The math for me is easy. So long as individual contributions are at least 6% of compensation, there is an additional 7.5% added. If that’s not free money, I’m not sure what is. My employer contribution comes in three forms:

- 3% of compensation, regardless of individual contribution (3%)

- 100% match for the first 3% of individual contributions (3%)

- 50% match for the next 3% of individual contributions (1.5%)

What does a “contribution” even mean?

There are two types of 401k contributions, “traditional” (pre-tax) or “ROTH” (post-tax). This Seeking Alpha article is halfway decent overview. Making traditional contributions ends up reducing your taxes owed in the year (i.e. the $23,500 I contributed reduced my taxable income by that amount). At some future point when you are taking withdrawals, you will pay taxes on the withdrawn amount. Making ROTH contributions is post-tax, but you end up paying no taxes on withdrawals at any point in the future.

Where does this money go?

Put simply, investments. Our provider, Fidelity, offers a range of different funds, target retirement date programs, indexes, and/or self-directed accounts to manage. My own contributions I split across two investments which largely track S&P500 and Russell2000 indexes. While it feels a bit ethereal to just be pouring money into something intangible, the reality is this is invested in businesses with the general goal of earning money.

I’m lucky to have the means to support this savings rate

For the past 5 years or so I’ve been lucky enough to be able to maximize individual contributions, and since month-1 of employment I’ve been able to max employer match. That adds up big, and at this point the funds in these accounts make up ~half of my net worth (and more than that as % of my investable assets, as there are things like homes and fancy cars in the mix there, too.) At some point in the future, likely in 20 years or so, I’ll start the long, slow draw on the 401k. These contributions now are likely enough alone to fund multiples of what retirement expenses will be. Pretty exciting position to be.

And the general takeaway is simple. Don’t leave money on the table with 401k or other savings programs. It can add up in truly meaningful ways.

And of course, a gif.