After an experience recently where I lost grace period by taking advantage of a promotional (non-zero) APR, I thought a post on the topic would make a fun and helpful reflection. The topic of interest-free period on purchases doesn’t often come to the front of credit card gaming conversation, but the reality is it’s actually a remarkably undervalued, legally protected benefit.

At current prevailing interest rates, this grace period is worth 0.23-0.49% additional earn rate on all purchases.

Grace period (see this CFPB article for a more comprehensive description)

Pay your card in full by the due date every month? Courtesy of the 2009 CARD Act, that comes with a required grace period for interest on any purchases. That means, so long as you’re not revolving, you get free “float” for these balances. That means you’re borrowing money temporarily, but not paying anything for it. The absolute best kind of borrowing.

Why it’s valuable

Until your payment due date, you keep your money in your own account. You can do whatever you want with that money (including not even have the money you may need to pay your bill in full), but for argument and analysis sake we’ll pretend like that allows you to keep that money in your own high-yield checking account. That means not only are you borrowing money for free, but you’re also earning interest on the money you’ve got stashed to pay that bill in the future. Quite literally, free money.

The math isn’t too complicated, but highlights how valuable this can be for cardholders

- This grace period is worth the equivalent of adding 0.23%-0.49% rewards earn rate to your card

- Here’s why:

- Keeping that money allows you to earn interest on the money to be used for that future card payment (!!!)

- While the rate of daily interest is low, depending on the timing of your purchase you can have up to 55-days of interest on your deposits (assuming your purchase posted on the first day of the statement) or a minimum of 25 days of interest on your deposits (assuming your purchase posted on your statement cycle date)

- Let’s do some quick math here to showcase this

- Interest rate of 3.25% yields a daily interest rate of 3.25%/365 = 0.0089%, or 8.9 cents for every $1,000 balance per day

- Scenario 1: $1,000 posts the day after your prior statement cycled (55 days of free borrowing)

- $1,000 x 0.0089% = $0.089/day x 55 days = $4.897

- $4.897 / $1,000 = 0.49% additional rewards value for purchase transaction

- Scenario 2: $1,000 posts on statement cycle date (25 days of free borrowing)

- $1,000 x 0.0089% = $0.089/day x 25 days = $2.315

- $2.315 / $1,000 = 0.23% additional rewards value for purchase transaction

- Assumptions:

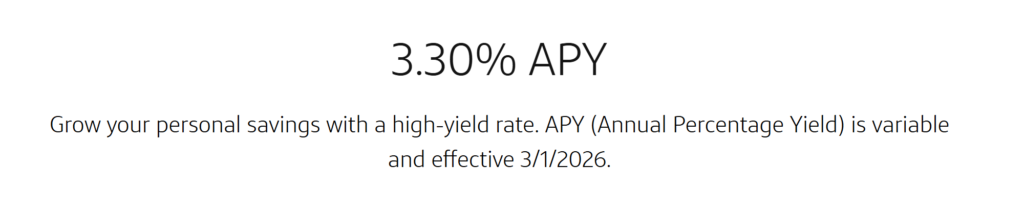

- High yield checking/savings rate of 3.25% rate (3.3% APY, or compounded interest rate)

- Grace period of 25 days (25 days between statement cycle date and due date)

- Payment made on the due date, but posts (withdrawn from the account) the day after the due date, allowing for interest on the payment due date

- Range of scenarios assumes purchase posting on the first day of the statement (the longest borrowing period) and the last day of the statement (shortest borrowing period)

- 30-day calendar month

- This is simplifying in that there is no assumption for compounding rewards, as well as there is no tax assumption for the interest on deposits, both of which will occur

Is this a complete game changer? No. But why leave money on the table, particularly if you’ve got big transactions planned where the scale is more worth any hassle!

Post-ending gif