I’m sitting on almost $600k in available credit across my various cards. I do take advantage of the occasional 0% promotion, but I have no need for the vast majority of that credit. That said, I do greatly enjoy testing out various experiences, and I also get a kick out of getting my cards some serious limits. Cue Discover.

I’ve been using my Discover card much more than normal

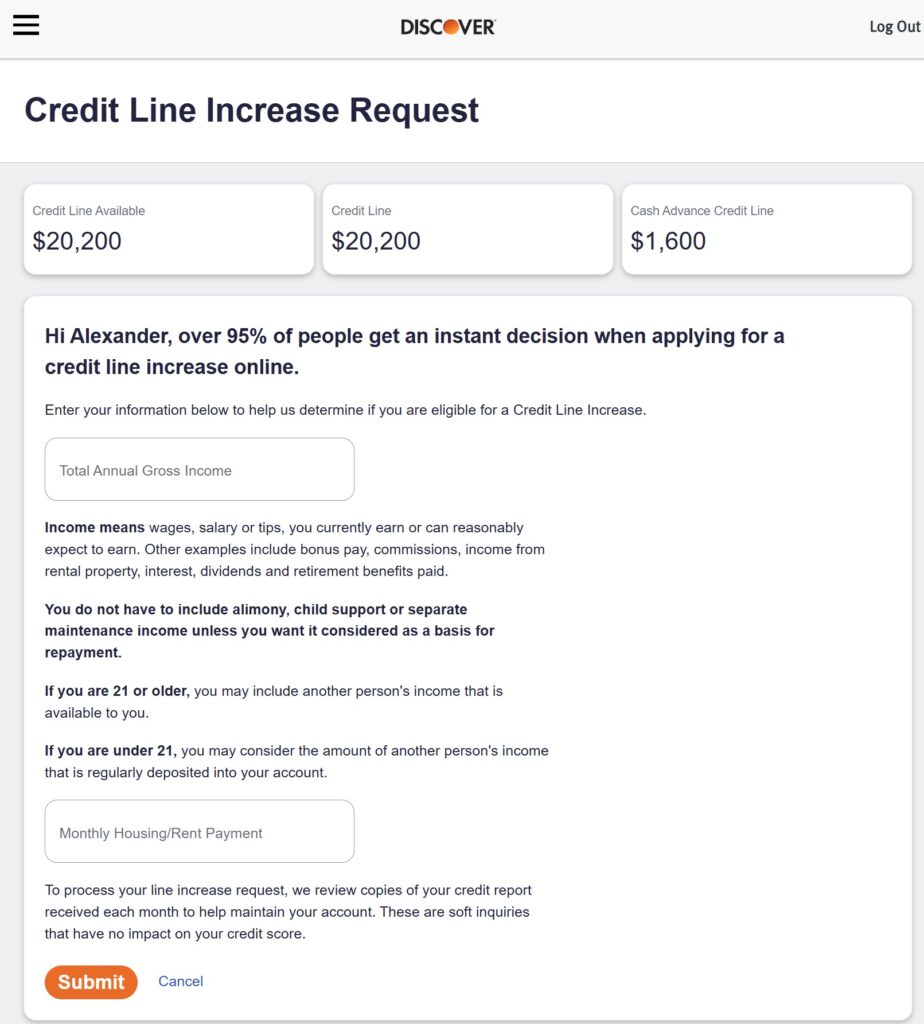

My typical activity on this card is limited (<$1,000 a month), and my limit is already more than sufficient at $19,500. That said, a month ago I took advantage of a 6.99%, no transfer fee balance transfer offer with most of my line (this rate is lower than my HELOC). That meant my utilization on this card was high, which can have an adverse impact on my credit score (it’s a signal of risk that my utilization on the one card is substantial.)

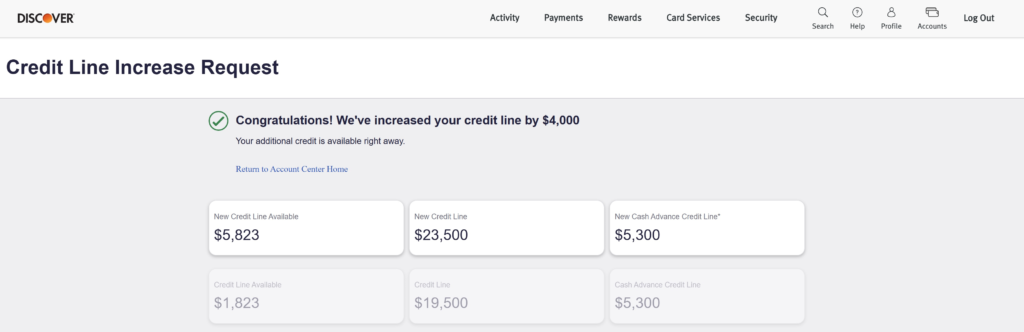

Discover instantly fulfilled a $4,000 increase on my Discover It card

Do I need it? No. Am I going to borrow or spend more as a result of it? No. Does it make me happy that I’m approved, and my utilization is now substantially lower on the card? Yes.

The page to request a line increase requests is simple, requiring only annual income and housing expense. Maybe five seconds after entering the info and pressing submit, I was granted an increase which is now live. This card has now grown from single-digit thousands to $23,500 over the more than a decade of holding the card. Loyalty pays, it seems.

Typically line increase requests have no hard inquiries, so there’s truly no downside to requesting. More credit is positive for your bureau, and means you have stronger evidence for responsible management. Take advantage because you can, so why not?

Post ending gif captures how I feel this Wednesday evening.