Anyone who knows me knows my very vocal position on sports betting. I won’t hash that here beyond describing the industry broadly as evil and predatory. Like any gambling, they get a good hook and get consumers to literally burn money. That makes the core foundation of this product also genuinely terrible. I hope G-Bank loses their shirt on this product by people taking advantage of them the way the industry takes advantage of consumers.

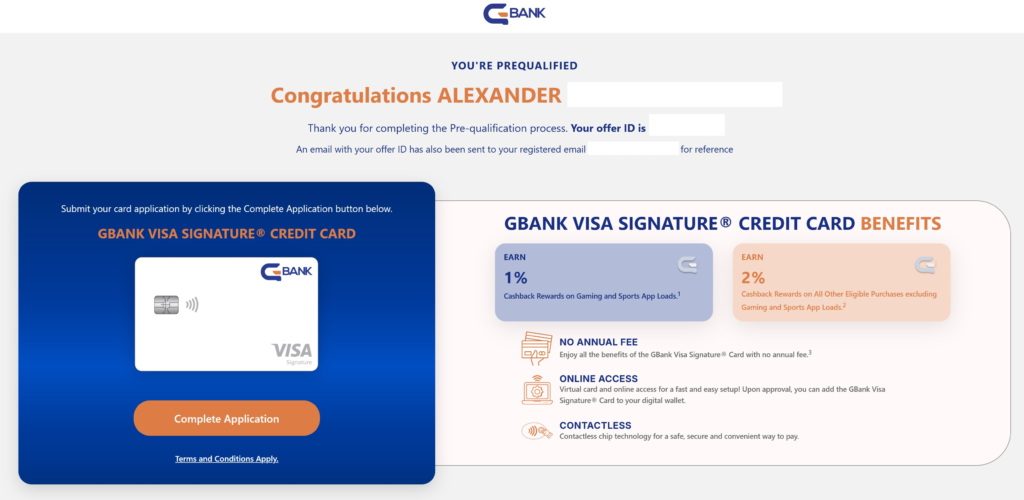

What is the card?

Simple and straightforward. No-fee, 19.24-27.24% APR, 2% cashback everywhere, 1% cashback (with no cash advance fees) on Gaming or Sports App loads.

What makes this special

No fee, 2% cashback everywhere is reasonably good, but is not something that’s earthshattering.

1% cashback on Gaming & Sports Betting with no cash advance fee is a highly unique. That’s a category that typically both charges cash advance fee and earns no rewards. The combination here is highly dangerous (ex. lets consumers bet on credit with no fee, which I would argue is very bad), but also potentially lucrative (see next section below).

How to be schemey

Assuming there is a reasonable credit limit on the card ($10k+), and one is funding sports betting accounts with the explicit aim of not gambling, and instead sitting on that cash/re-depositing to one’s own bank account, you pocket that 1%.

The math can be quite simple: $10,000 funded to Sports Betting account via card load, $10,000 x 0% = $0 Cash advance fee, $10,000 x 1% = $100 Rewards

The math can also be more exciting: $10,000 funded to Sports Betting account via card load, $10,000 x 0% = $0 Cash advance fee, $10,000 x 1% = $100 Rewards; $10,000 withdrawn & deposited in a 3.25% Rate (3.3% APY) HYSA for 35 days = $31.16 interest = $131.16 total value

The real questions are 1) which Sports Betting accounts would allow large card based funding and easy withdrawal without bets, 2) how long would it take to have G-Bank shut down the account?

Post-ending gif