As one might expect of me, I push my relationships with every financial institution and expect perfection in delivery. Unsurprisingly, this often leaves me disappointed and escalating for attention with limited results. Cue the CFPB (Consumer Financial Protection Bureau). While they were chartered for bigger and better things (read: enforcement and regulation to protect consumers) their function has been paired back heavily in the most recent administration to supporting escalated complaints. While a shell of their former self, this is an incredibly important function.

Complaints complaints complaints!

The complaints function itself is remarkably simple. While the complaint itself is little more than a web based form and upload, this effectively triggers immensely escalated attention and focus from any receiving bank. I have found this to be an effective last line of escalation, and typically yields the right customer outcome.

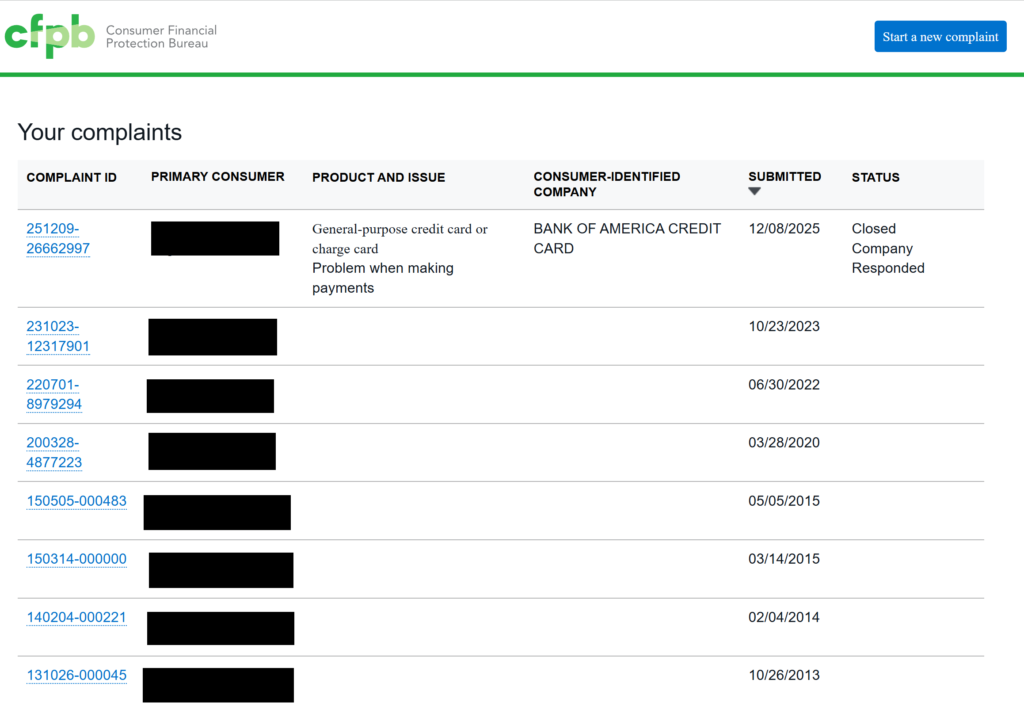

Turns out, I’ve filed a few complaints since the CFPB launched. And while I don’t remember every individual complaint, I do know that multiple outcomes have been meaningful in addressing bank issues. Since 2020 these include…

- Bank of America – misapplied payment & assessed interest charges (2025)

- Bank of America – mortgage application fee charged inappropriately (2023)

- Truist – Bank failed to pay real estate taxes on time & fees assessed (2022)

- American Express – 100,000 Membership Rewards points from sign up bonus did not fulfill (2020)

This is a valuable tool to hold banks accountable and ensure they treat customers fairly and fulfill commitments appropriately. While it in and of itself doesn’t guarantee that, I think it’s an important tool and I can personally evidence the action taken as a result of these complaints.

Cue my recent experience

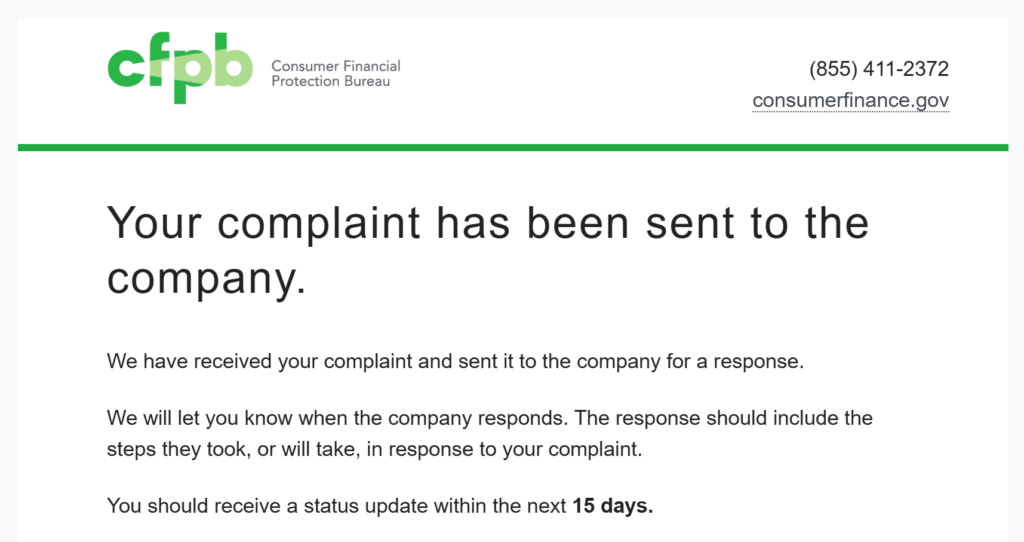

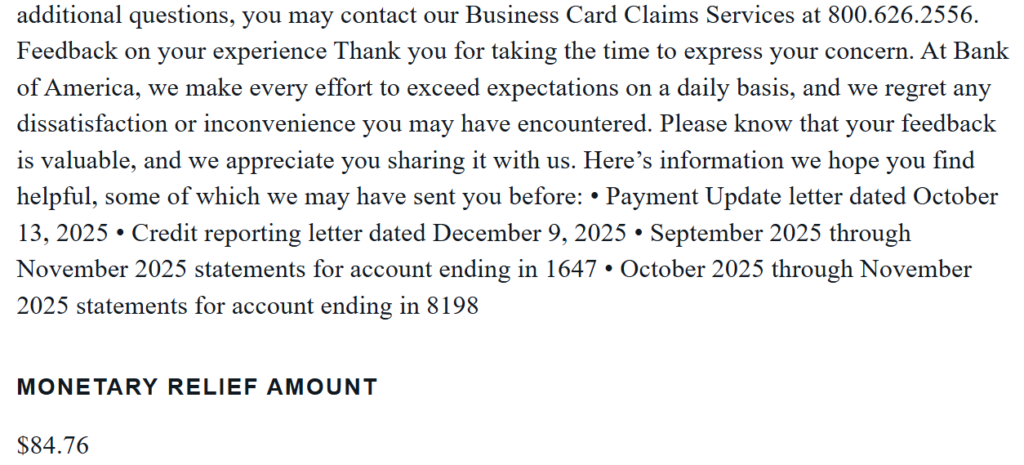

Earlier this month I filed a CFPB complaint after being told by customer service there was nothing they could do to support or escalate my claim. By 9AM the morning after my CFPB complaint I had received a phone call from Bank of America, and a week later I have a letter from them and a refund in my account. It’s not huge ($84.76), but I was so peeved at the experience, I felt like complaining would bring me some mental relief (and it brought some nominal financial relief, too.)

What happened?

The root of this is a new Bank of America card I opened up in the fall. Stellar promotion for Alaska Airlines with 80k miles and a companion pass for a month’s worth of spending. Apply, approved, spend, great. Unsurprisingly, when you spend money there is an expectation you pay it back. So when my bill was due, I went online, clicked “bill payment”, and made a payment. Well, the reality of Bank of America systems is they’re archaic. Turns out, even though I clicked bill pay, and the top internal account showing was an Alaska Airlines Visa Signature card, that was an old account and not the current account. But the money was out of my checking, and everything looked fine until I got a missed payment notification from Bank of America.

Customer Service folks have a hard job, and I don’t envy being on the receiving end of a “what the hell” conversation with me. They were helpful, opened a ticket to troubleshoot, refunded the late fee, and indicated they would follow-up. They did, and in that ticket escalation they refunded the payment to the wrong card account, resulting in a multi-thousand dollar balance continuing to accrue interest. That was a whole thing to get a credit balance refund, deposit it in my account, pay the card again, etc.

In the end, I had two interest charges as a result of this payment issue that the internal escalation WOULD NOT refund. The obnoxious part about ever paying interest in a month (or missing a payment) is the pesky loss of grace period (no interest period) and residual interest charges. So despite shifting money around and paying the balance in full, the next month I had interest charges again. Quite annoying.

That residual interest was the trigger for me to file a complaint. I asked for a grace period reset, they denied it. So instead BofA gets to spend way more money managing a complaint and still giving me the financial remediation I was originally requesting.

If the rewards weren’t so good, I’d for sure be through with BofA.

Obligatory post-end gif