Tax day is going to be a bit rough in our household. It’s looking like I’m going to owe a few thousand, which always is a bit of a sucker punch (despite being entirely expected.) After owing for many years, I’ve learned how to take advantage of these exceptionally large, known expenses. Extra rewards? Sign me up. Extra float on a 0% promotional rate card? Absolutely.

You can in fact pay your Federal tax bill with a credit card

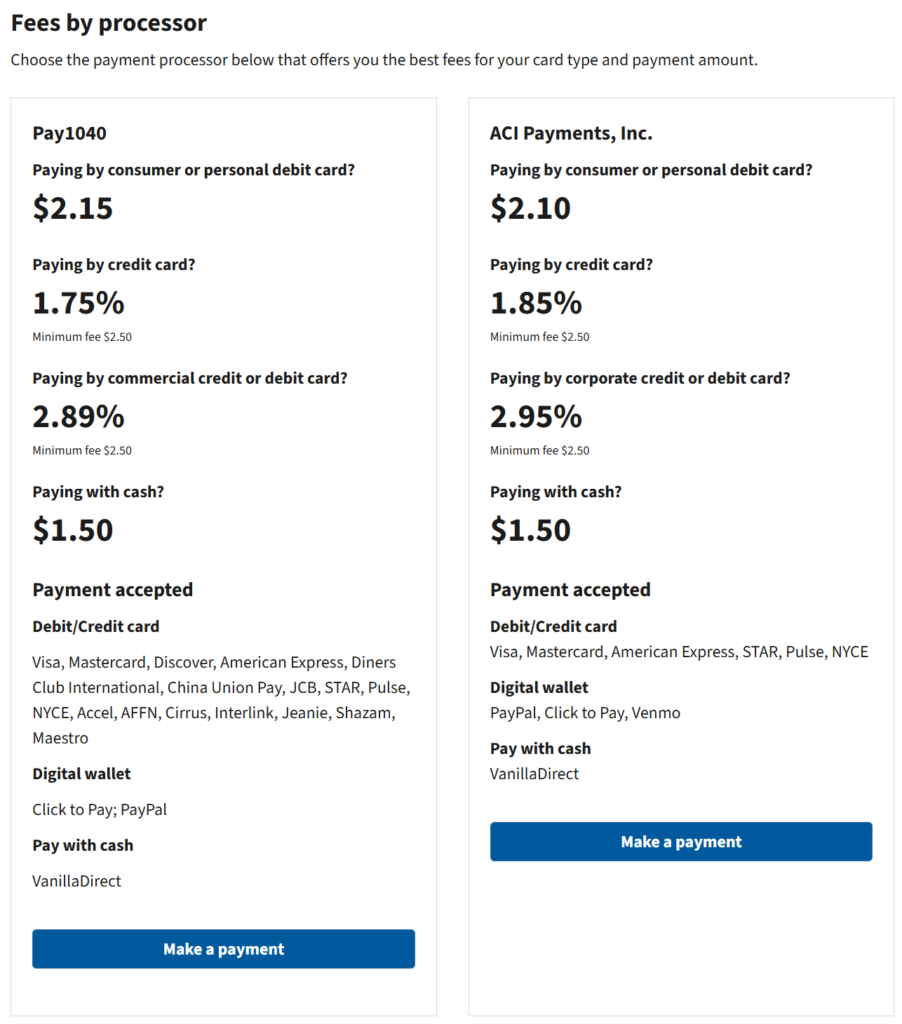

There are two payment options in 2026 now available, down from three in 2025. Admittedly I have only used the provider that is no longer available. In making payments, the only issues I ever had were on the IRS front. Pay1040 offers credit card tax payments for 1.75%. ACI Payments offers credit card tax payments for 1.85%. If your card earns more than this, there’s some effectively “free” rewards in your pocket.

My strategy is a mix of early spend bonuses and extended 0% promotional rate float

A month or so ago I shared a post about a few new cards I signed up for. The intent behind those sign-ups was partly to take advantage of known future spend for bonuses, and to leverage 0% promotional rates to stretch out the effective cash-flow impact of taxes out over a few months. With high yield savings accounts still yielding in the 4% range, there’s some meaningful benefit of holding cash. With that said, here’s my plan:

- Close out the JetBlue Plus early spend bonus ($1,000 spend for 70,000 points)

- Close out the Truist Business Cash card spend bonus ($3,000 spend for $300 cash) and use the 9 months of 0% purchase rate APR for extended repayment

- Reminisce about using my Bank of America Cash card to earn 5.25% on tax payments (capped $2,500/quarter, 3% “online purchases” +75% loyalty bonus = 5.25%)

Don’t leave money on the table.

- Illustrative example highlighting value/cost for a $1,000 tax payment

- $1,000 tax bill payment ($1,000)

- 1.75% convenience fee ($1,000 x 1.75% = $17.50)

- Total charged to credit card: $1,000 + $17.50 = $1,017.5

- 2% credit card rewards ($1,017.5 x 2% = $20.35)

- Net value: $20.35 (rewards) – $17.50 (fees) = $2.85

- This example gets much more interesting when you also add in a month of free float from using a card, and parking that tax money in a high yield savings account

- **bonus** $1,017.5 x 4.00% return / 12 = +$3.39 HYSA interest

- Bonus net value: $2.85 (illustrative example value) + $3.39 (interest) = $6.24

Are you going to get rich with this? Surely not, as you’re immediately poorer as a result of paying taxes. But you can claw some of those expenses back through extra rewards, or easily hit the early spent bonus for that fancy new card you just signed up for! At a minimum, it’s worth considering.

Post-ending gif