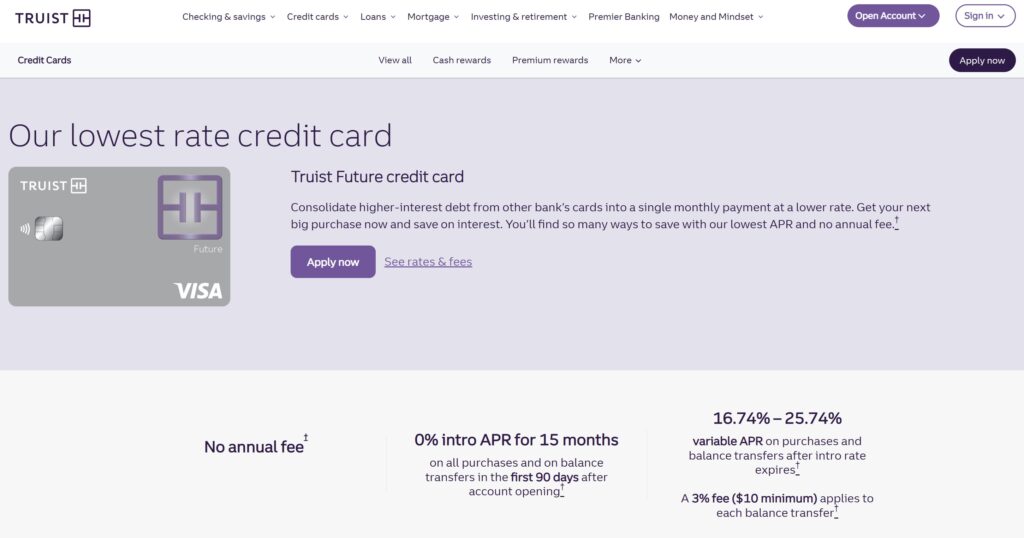

Because I made a big mistake in my finance tracking, I just paid $115.34 in interest on my Truist Future card. In my finance tracking spreadsheet I noted September’26 as the purchase rate promotional expiration, but I was many, many months off. Despite having the funds parked in a high yield savings account, when the promotional APR expired after my March’26 statement, I was bumped up to brutal 16.74% APR on an ~$8,000 balance. Not a great feeling just straight burning that cash. There are some takeaways here both on how to use these to your advantage, and how not to make the same mistake I did.

0% promotional rates are amazing tools

Whether it’s a purchase 0% or a balance transfer 0%, getting cheap or free float for an extended period of time is amazing. While spending money you don’t have is never a good idea, this helps smooth out the repayment of expenses. In my own instance, I had a big tax bill and vet bill at the same time in early 2025. The 0% promotional rate helped me avoid a big payment shock of these expenses, and instead repay the balance over an extended period of time, but without substantial interest charges. There are so, so many 0% promotional rates for new cards, if there are large expenses you almost can’t avoid having the option of the flexibility.

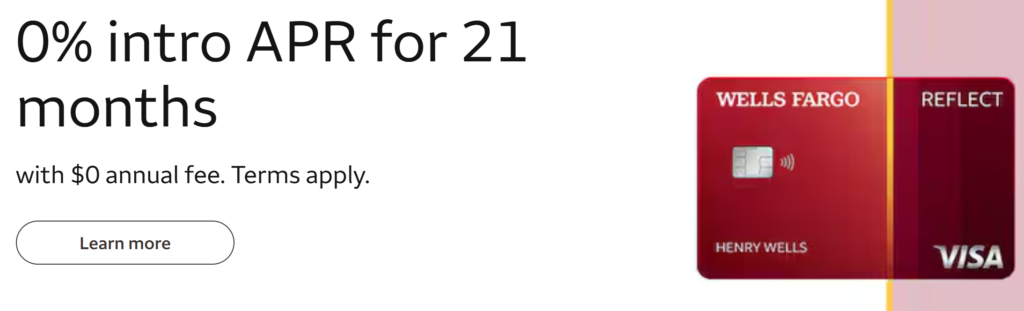

Looking only at Wells Fargo, you can find a range of offers with different durations and balance types eligible for promotional rates:

- Active Cash – offers 0% for 12 months on purchases and balance transfers

- Autograph – offers 0% for 12 months on purchases

- Reflect – offers 0% for 21 months on purchases and balance transfers

When promotional rates expire, there’s no more promotional rate (shocker)

0% is a great interest rate. 16.74%, not so great. This end of promotional rates greatly increases required payments, in my own instance from $81 (1% of balance) to $196 (1% of balance + fees/interest charges). Given my high yield savings account yields only 3.5%, I quite literally burned $100 as a result of my error. Not the end of the world, but certainly not ideal.

I contacted Truist and asked for an interest waiver, but I was not eligible

The truth is that I made a mistake. The end outcome here is I paid for that. They shared the waiver policy for interest charges requires full payment for the preceding three statement cycles, and because I was making near-minimum payments, I was not eligible. Despite escalating to a supervisor, the apologize-and-beg strategy was unfortunately a waste of my time. Bummer.

As a thank you to Truist for not having a better policy for customers, I took a few minutes this evening to sign up for a new checking account where they’ll pay me $400 for a nominal deposit. While I’ll be “whole” in about a month as a result, the mistake here still stings.

Lesson learned, the hard way. Plan and document appropriately to avoid missing full repayment before 0% expiration. Don’t be a sucker like me.

Post-ending gif