Every so often I stumble across an offer that makes me think, “no, that can’t be right”. As I look deeper to understand the gimmicks and gotchas, that offer becomes even more outrageous, and also somehow confirms the genuine and impressive nature of the offer. This offer from Venmo (Paypal) is just that. 6-month enhanced earn rate, tripling the earn offered by the card. Even the non-enhanced 3%-everywhere is impressive (1% x 3). The variety of categories is strong. The 6%-second spend category is insane value (2% x 3). The 9%-top category is downright maniacal (3% x 3). The cash back offered by this card is unparalleled, and there is no reason not to take advantage.

This is the best new card offer I have ever seen.

The Venmo Credit Card Offer (link)

- The base Venmo Credit Card is perfectly fine, but not impressive. It offers 3% in top-spend category, 2% in second-spend category, and 1% everywhere. Uncapped, automated, auto-redeemed to Venmo balance.

- The promotional Venmo offer is wild. It is the same base product (3/2/1), but offers triple-earn across each of these during the 6-month promotional duration. 9% in top-spend category, 6% in second-spend category, 3% everywhere. Uncapped. Each of these is generally a best-in-class earn rate, particularly so for cash rewards.

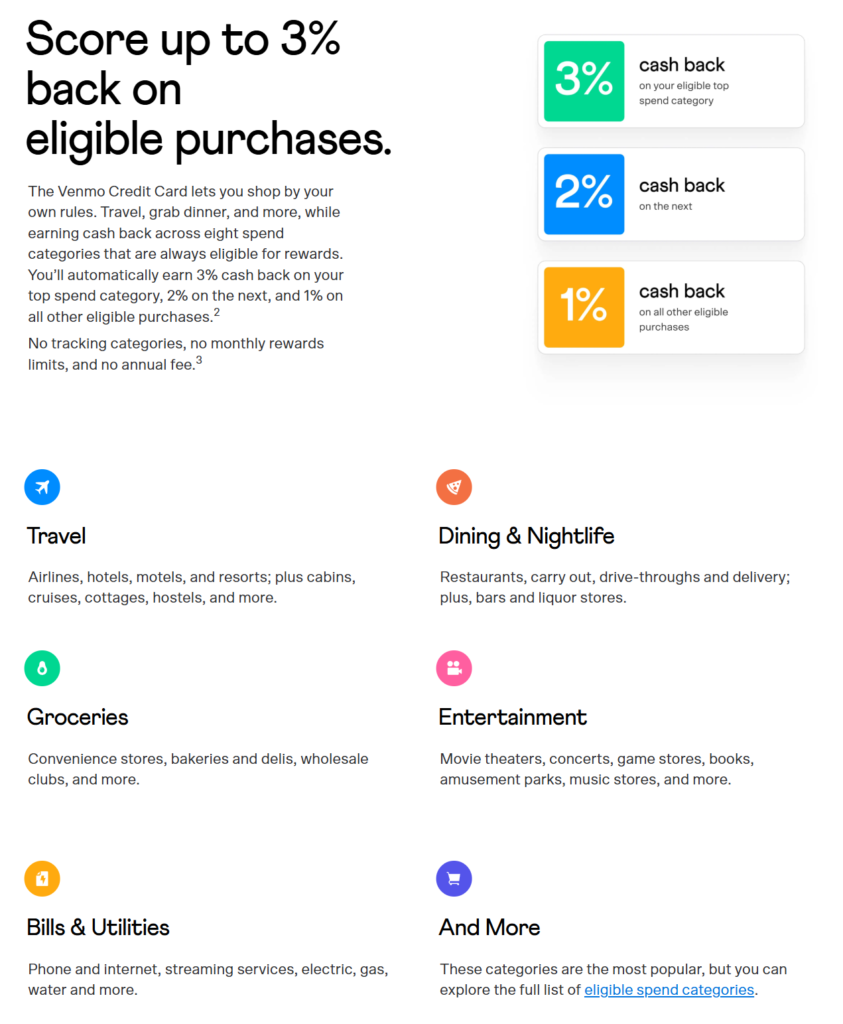

- The challenge to value is the available categories for spend, and whether those 9% and 6% are actually useful. There are eight eligible enhanced earn categories listed, and each of the examples feels like there is value for the right customer.

- Travel

- Groceries

- Bills & Utilities

- Dining & Nightlife

- Entertainment

- Transportation

- Health & Beauty

- Gas

- To find if you are available, check your email for a targeted message, or go into your Venmo app, click “Cards”, and swipe to “Credit”

My Take

- If there’s one card to get, have, and use for the next six months, it’s this.

- Base earn reflection: 3% base earn in cash is insane, everywhere, low complexity value. The widely available 2%-cash offerings can’t compete.

- Enhanced earn reflection: 9% top-category and 6% second-category earn in cash is absolutely mind blowing. Even looking at typical consumer spend, this presents wild value back to the cardholder. On top of that, considering how one can abuse the offer & maximize value (ex. get 9% enhanced earn at the grocery store purchasing visa gift cards), this can effectively translate into ~8% cash back across all spend.

- Venmo is a legitimate business and Synchrony isn’t some second tier fintech startup. They have the funds to make good and pay up, and aren’t closing up shop. Worst case, CFPB complaint triggers review & escalation.

- The terms & conditions do reflect that rewards are earned on statement cycle and transferred to Venmo account following that. If the account is closed by the consumer OR Synchrony, that any rewards earned are forfeit. Don’t abuse the enhanced earn too much, or else.

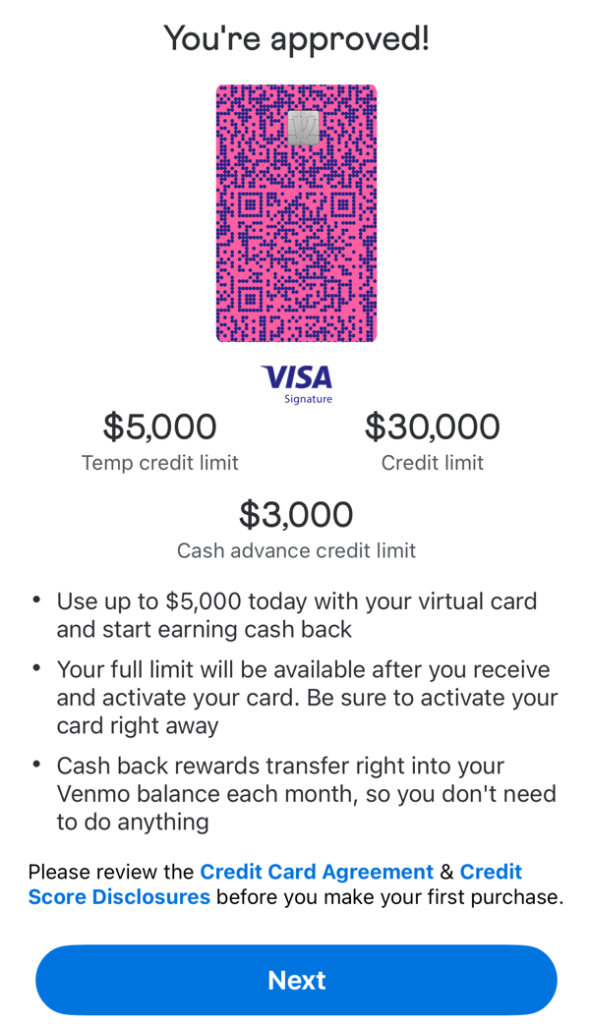

- They do offer solid credit lines (they approved me for $30k!)

My plan

- Sign up for the card

- Maximize the 9% enhanced-earn category as follows:

- Personal spend: Move vast majority of my card-based spend to prepaid Visa gift cards purchased from Kroger (Grocery Store category earning 9%, with a ~1% prepaid card purchase fee) || ~$4,000/month spend across personal & home budget

- Tax payments: Make quarterly estimated tax payments for 2026 taxes, using $500-increment Visa Gift cards (same net-8% as above) || ~$1,000/month spend

- Manufactured spending: Load up on Visa Gift Cards from the grocery store and cash out with one or multiple of the following methods (will assess all of the following over the coming month) || ~$10,000/month spend

- Make HELOC payments via debit card (0% fee to make payment using debit)

- Purchase & deposit money orders (~0.2% fee to cash out)

- Make P2P payments using Venmo/Paypal/Other (~2-3% fee)

- Purchase USD crypto using debit card, transfer to checking (~2.5% fee)

- Sign up for a payment terminal and cash out debit cards using network (~2-3% fee) — given tax implications of this, this is likely not the route I will go

- Work hard to not trigger fraud/abuse protections from Synchrony/Venmo so I can keep the schemes running for 6-months

- Redeem absolute boatloads of rewards, offsetting any card purchase fee expenses

- Here’s what I’m thinking is achievable without working too hard:

- Spend: $15k x 6 = $90k ($4k + $1k + $10k spend outlined above)

- Rewards: $90k x 9% = $8.1k (grocery store top-category)

- Fees: $90k x 3% fees = $2.7k (card purchase + cashout fees)

- Profit: $8.1k – $2.7k = $5.4k profit (~$900/month, or ~$30/day for the next 6 months)

- Write a post to share my experience on the tail end of this outrageous, entertaining and lucrative adventure

Post-ending gif (a manifestation of me in 6-months)